Manulife John Hancock Retirement published its Financial Resilience and Longevity Report that offers insights into retirement preparedness to help individuals across generations approach their retirement years with confidence. The report identifies the reverse mortgage line of credit as a potential source of retirement funds.

BIGGEST TAKEAWAYS FROM THE REPORT

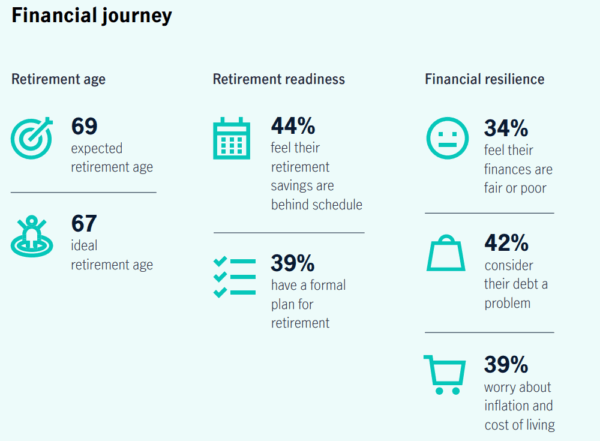

- Retirement is lasting much longer—potentially 40+ years

Life expectancy is rising, more people are living past 100, and over half of retirees stopped working earlier than planned—causing retirement to last decades longer than many anticipated.

- Early, unexpected retirement is common—and financially disruptive

- 52% retired earlier than planned (average age 56).

- 70% of early retirees did so for health or family illness, not choice.

- Early retirees are far more financially stressed and more likely to rely solely on Social Security.

- Retirement is significantly more expensive than retirees expected

Retirees were surprised by:

- How fast savings were depleted

- Large unexpected expenses

- The impact of inflation on daily living costs

- Many wish they had saved more, earlier.

- Retirees overwhelmingly stress the importance of planning early

Their strongest messages:

- “Retirement may come sooner than you think.”

- “Even small contributions, started early, matter.”

- “Have a real plan—not just a mental outline.”

- Financial planning and professional help matter

Retirees who had a formal plan before retiring:

- Felt less stressed

- Had more income sources

- Adjusted better to unexpected changes

- Working with a financial advisor was one of the most common pieces of advice.

- Retirement readiness differs dramatically by generation

Each generation is stressed, but for different reasons:

- Gen Z – Struggling with basics; retirement feels distant.

- Millennials – Most financially stressed and most behind on retirement savings.

- Gen X – “Sandwich generation”; high caregiving costs and low savings.

- Boomers – Most confident but still concerned about longevity risk.

- Financial stress is widespread—even among workers—and affects well-being

Workers spend 4.6 hours a month dealing with personal finances at work and 16 percent miss work due to financial stress. This indicates retirees and pre-retirees are feeling more strain than in past years.

ACTIONABLE ITEMS FOR RETIREES

Below are practical steps retirees (or near-retirees) can take based on the report’s findings and retirees’ real-world experiences.

- Plan for a much longer retirement horizon—30 to 40 years or more

- Assume your savings must last longer than you expect.

- Revisit withdrawal strategies regularly.

- Consider income sources that provide guaranteed lifetime payouts (annuities, pensions, Social Security optimization).

- Prepare for the possibility of unexpected early retirement

Since illness or caregiving forces many to stop working earlier:

- Build a larger emergency fund (12–24 months).

- Identify backup income sources (e.g., part-time work options, home equity strategies, reverse mortgage line of credit).

- Review disability and long-term care coverage before leaving the workforce.

- Strengthen your retirement income plan

Retirees wish they had:

- Saved more

- Diversified better

- Planned for unexpected expenses

Action steps: - Create or update a formal retirement income plan, including:

- Income sources

- Withdrawal strategy

- Required Minimum Distributions

- Tax planning

- Stress-test your plan for inflation spikes, market downturns, and major expenses.

- Work with a financial professional you trust

Retirees strongly recommend this. A professional can help with:

- Social Security claiming strategies

- Tax-efficient withdrawals

- Investment allocation for longevity

- Healthcare and long-term care planning

- Estate planning

- Consider annual or semiannual reviews.

- Budget for rising costs—especially healthcare and inflation

Retirees were caught off guard by:

- Inflation

- Medical expenses

- Home/car repairs

Action steps: - Build a budget that includes rising healthcare costs (Medicare premiums, supplemental insurance).

- Increase your contingency fund for home/auto repairs or caregiving needs.

- Track spending quarterly to adjust early.

- Diversify income beyond Social Security

Early retirees relying solely on Social Security had the most financial stress. Additional income sources may include:

- Part-time work (flexible, low-stress roles)

- Rental income

- Dividend or interest income

- Reverse mortgage credit lines

- Annuity payments

- Plan intentionally for your time, purpose, and social life

Retirees said that after 2 years, the “honeymoon phase” wears off. They recommend:

- Creating a weekly schedule with activities, hobbies, and social commitments.

- Joining local groups, volunteer, or take classes.

- Staying physically active and mentally engaged.

A structured lifestyle helps prevent depression, boredom, and isolation.